Introduction

Running a fixed asset audit should not feel like a year-end fire drill. If your team is still chasing spreadsheets, hunting missing assets, and explaining register mismatches to auditors at the last minute, this guide will help you turn fixed asset auditing into a repeatable control process.

A fixed asset audit systematically reviews property, plant, and equipment to confirm that assets exist, match their recorded locations, belong to the business, and reflect accurate records in the fixed asset register and financial statements. Many organisations rely on asset verification software to support this process with consistent data capture and validation. A strong fixed asset audit also checks depreciation inputs, transfers, disposals, supporting approvals, and the control trail behind each change.

In this guide, you’ll learn:

- What a fixed asset audit really involves, and how physical assets, your register, and financial records should all line up.

- Why these audits matter more than ever, especially as assets move across teams, locations, and systems.

- How to run an audit step by step, including what to check, how to verify, and how to handle gaps.

- Finally, how to make audits easier going forward, with better controls, clearer ownership, and the right use of software.

What is a fixed asset audit?

A fixed asset audit is a review of long-term tangible assets and the records behind them. In practice, the audit combines physical verification, register validation, accounting checks, and control testing.

That matters because a physical sighting alone is not enough. A tagged laptop can still sit in the wrong cost center. A machine can exist on the shop floor yet remain recorded with the wrong location, incorrect useful life, or an inaccurate status in the fixed asset register. Likewise, a disposed asset can remain on the books long after it has left the site.

Why fixed asset audits matter in 2026

Fixed asset audits matter because asset risk now sits at the intersection of finance, controls, and operations. Teams no longer manage assets in one building and one ledger. They manage equipment across plants, offices, project sites, remote users, repair vendors, and customer locations.

As a result, the biggest fixed asset problems are rarely accounting-only problems. They usually show up as cross-functional breakdowns, such as:

- Assets get moved, but the register is not updated, so records quickly become unreliable.

- Disposals are completed on the ground; however, finance records are not updated accordingly.

- Over time, ERP data and field records start drifting apart, which creates confusion during audits.

- Meanwhile, IT or plant teams use different asset identifiers, making it harder to match them with the fixed asset register.

- As a result, periodic audits highlight issues, but no one takes clear ownership to resolve them afterward.

From a finance perspective, bad asset data can distort additions, depreciation, impairment indicators, and disposal accounting. And from an audit perspective, weak asset records create avoidable questions around existence, completeness, authorization, and record accuracy. From an operations perspective, poor asset visibility hides idle stock, lost equipment, duplicate purchases, and uncontrolled movement.

In 2026, the best fixed asset audit programs do not wait for year-end. They create a year-round evidence trail that makes year-end easier.

The AssetCues audit-ready evidence stack

Most teams think about a fixed asset audit as a single event. A better way to manage it is to think in layers of evidence.

The AssetCues audit-ready evidence stack is a practical model for building fixed asset confidence from the register up to the final report.

Layer |

Core question |

Typical evidence |

|---|---|---|

| 1. Register integrity | Is the master record complete and usable? | Asset ID, class, description, cost, date-in-service, location, custodian, status |

| 2. Identity proof | Can each asset be uniquely identified? | Barcode, RFID tag, serial number, equipment number, plate number |

| 3. Physical proof | Can the team prove existence, location, and condition? | Scan record, photo, timestamp, geo-tag, field note, custodian confirmation |

| 4. Accounting proof | Does finance reflect reality? | FAR-to-GL reconciliation, capitalization support, useful life data, and disposal entries |

| 5. Control proof | Were lifecycle events authorized and logged? | Approvals, transfer forms, disposal approvals, movement logs, exception workflow |

| 6. Reporting proof | Can management act on the findings? | Coverage summary, exception report, financial impact, remediation tracker, sign-off |

This model matters because each layer answers a different risk. A scan solves one problem. It does not solve them all.

Why this model works

- It separates physical evidence from accounting records, making the distinction clearer.

- As a result, the internal audit gets a more structured and understandable control narrative.

- At the same time, finance teams can see why a simple count is not enough to close the file.

- Ultimately, reporting becomes more actionable, since each exception is directed to the right layer.

What does a fixed asset audit check?

A fixed asset audit usually checks more than whether an asset is physically present. It should test the accuracy of the full lifecycle.

Area checked |

What the team is asking |

Typical evidence |

|---|---|---|

| Existence | Is the asset real and in service? | Physical sighting, scan, photo, serial match |

| Completeness | Are all real assets recorded? | Floor-to-file review, receiving records, site walk |

| Location and custodian | Is the asset where the register says it is and assigned correctly? | Site verification, user confirmation, and movement records |

| Ownership or rights | Does the business have rights to the asset? | Purchase record, lease support, title, or asset file |

| Valuation support | Is the asset cost basis supported? | Invoice, capitalization memo, project completion support |

| Depreciation accuracy | Are the useful life, method, and in-service dates correct? | Register fields, depreciation run, policy mapping |

| Condition and impairment signals | Is the asset damaged, idle, obsolete, or impaired? | Condition note, maintenance logs, management review |

| Transfers and disposals | Were movements and retirements recorded correctly? | Transfer forms, disposal approvals, sale or scrap evidence |

| Control trail | Were changes approved and logged? | Workflow approval, audit log, access controls, exception tracker |

A practical rule

A fixed asset audit should answer both directions of testing:

- Books to floor: Everything in the register should be traceable to reality.

- Floor to books: Every material in reality should be traceable to the register.

When teams only test one direction, they often miss either ghost assets or unrecorded assets.

How to conduct a fixed asset audit

The most reliable fixed asset audits follow a structured flow. The exact level of testing will vary by asset class, geography, and materiality. Still, the core process stays consistent.

A strong fixed asset audit goes beyond basic checks—it connects scope, clean data, physical verification, and reconciliation to uncover real issues, not just surface gaps. It then turns those findings into clear actions with defined ownership and impact, ensuring problems are resolved and do not repeat.

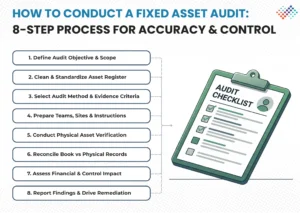

Step 1: Define the audit objective and scope

Start by stating what the audit must prove.

Examples:

- Support year-end financial close.

- Prepare for a statutory audit or an internal audit.

- Validate assets after a merger, relocation, or ERP migration.

- Clean the register before software rollout.

- Review high-risk classes such as laptops, plant machinery, vehicles, or field tools.

Then define scope:

- Define the asset classes clearly, so the audit focuses on the right set of assets.

- Include all relevant locations as well, ensuring no site is left out of the scope.

- Specify the legal entities involved, especially when multiple units operate under different structures.

- Set book-value thresholds carefully, so the team prioritizes high-impact assets.

- Decide the audit approach too, whether you will conduct full verification, sample testing, or an exception review.

A vague scope creates vague findings. A clear scope makes coverage measurable.

Step 2: Clean the fixed asset register before fieldwork

Do not send teams into the field with a broken register.

>Before fieldwork, standardize:

- Unique IDs.

- Descriptions.

- Location hierarchy.

- Custodian fields.

- Asset status.

- Capitalization date.

- Useful life.

- Disposal flags.

This is also the point to identify obvious duplicates, blank identifiers, retired assets still marked active, and assets with no known location.

Step 3: Choose the audit method and evidence standard

Next, decide how evidence will be captured:

- Wall-to-Wall.

- File-to-Floor.

- Floor-to-File.

- Cycle count.

- Sighting Audit.

- Hybrid.

Also, decide the minimum evidence standard. For example:

- Scan plus photo for movable assets.

- Serial number confirmation for IT assets.

- Location tag plus condition note for plant equipment.

- Document-plus-physical proof for leased or shared assets.

This step matters because teams often over-verify low-risk assets and under-document high-risk ones.

Step 4: Prepare sites, teams, and audit instructions

Field execution fails when the operating model is unclear.

>Before starting:

- Assign clear owners for each site or asset class, so accountability is established from the start.

- Brief the field teams properly, ensuring they understand the classification rules before execution begins.

- Explain how to handle exceptions as well, including missing, moved, scrapped, or duplicate assets.

- Define escalation paths in advance, so teams know exactly whom to contact when issues arise.

- Confirm cut-off rules clearly, ensuring everyone follows the same approach for assets received, moved, or retired during the audit period.

At this stage, good teams also prepare exception codes so findings stay consistent across locations.

Step 5: Perform physical verification

Now, verify the assets in the field. For each asset, collect the agreed proof:

- Identifier match.

- Location confirmation.

- Custodian or department condition.

- Supporting evidence such as a scan, a photo, or a note.

For remote, customer-site, or field assets, you may need alternate evidence such as:

- Custodian confirmation.

- Service logs.

- Geo-tagged photo proof.

- Supervisor confirmation plus follow-up verification.

That is why physical audit design should match the operating reality of the asset base.

Step 6: Reconcile differences in both directions

After fieldwork, reconcile the results:

- Identify assets listed in the books but not found physically, so gaps become visible.

- Capture assets found on-site but missing from the records, ensuring nothing is left unrecorded.

- Check for location or custodian mismatches as well, so ownership details stay accurate.

- Review asset class and descriptions carefully, ensuring they reflect the correct information.

- Flag assets that are physically present but no longer active, so records stay relevant.

- Track assets that were disposed of operationally; however, not removed from finance records, so discrepancies can be resolved.

This is where the real audit value appears. A fixed asset audit becomes useful when the team turns raw field exceptions into accounting and control actions.

Step 7: Quantify financial and control impact

Not every discrepancy has the same consequence.

Classify findings by impact:

- Start by evaluating the financial statement impact, so you understand how discrepancies affect reporting.

- Then, identify any control weaknesses, ensuring gaps in processes are clearly highlighted.

- Look at operational issues as well, so day-to-day inefficiencies are not ignored.

- Assess data-quality problems carefully, ensuring records remain accurate and reliable.

- Finally, flag any policy non-compliance, so corrective actions can be taken in time.

For example:

- A missing low-value chair may be an operational control issue.

- A disposed machine that still depreciates in the ledger is a financial issue with direct reporting impact.

Separating these effects helps management respond properly instead of treating every exception the same way.

Step 8: Report findings and assign remediation

Finally, issue a report that does more than list exceptions.

A useful report should:

- Start by stating the coverage achieved, so stakeholders clearly understand what was reviewed.

- Summarize the method used as well, ensuring the approach is transparent and easy to follow.

- Quantify the different types of exceptions, so the scale of issues becomes visible.

- Identify the likely root causes, helping teams understand why the issues occurred.

- Estimate the financial impact where relevant, so the business can assess the risk.

- Assign clear remediation owners, ensuring accountability for fixing the issues.

- Finally, set due dates for closure, so actions are tracked and completed on time.

Without ownership, the same findings return next year.

Which audit method should you use?

There is no single best method for every asset environment. The right method depends on mobility, value, control risk, and site complexity.

Method |

Best for |

Strength |

Limitation |

|---|---|---|---|

| Wall-to-wall | Plants, warehouses, and offices with high asset density | High visibility and strong completeness coverage | Resource-intensive |

| File-to-floor | Statutory or external-audit support | Good for existence testing from the register | Can miss unrecorded assets |

| Floor-to-file | Register cleanup projects | Good for finding unrecorded assets | Needs strong field judgment |

| Cycle count | Large distributed populations | Spreads workload across the year | Requires disciplined scheduling |

| Sighting audit | Remote, branch, field, and customer-site assets | Efficient existence and location confirmation | Often needs alternate evidence rules |

| Exception-led re-verification | Mature environments with prior data | Focuses effort where risk is highest | Depends on strong prior data quality |

| Continuous software-led verification | High-change environments | Builds year-round audit readiness | Requires process discipline and tools |

A simple selection guide

1. Use wall-to-wall when:

- Use a wall-to-wall approach when the asset register is weak, as a full check helps rebuild accuracy.

- Apply it for high-value sites as well, so critical assets are thoroughly verified.

- Consider it when management needs a reset, ensuring records and controls are brought back on track.

2. Use file-to-floor when:

- You can rely on the register for most records, as it is generally accurate.

- However, you still need to strengthen the audit evidence, so it holds up during reviews.

3. Use cycle counts when:

- The asset base is large and widely distributed, so teams must plan coverage carefully.

- It also remains operational throughout the year, which means you need a continuous and well-coordinated approach.

4. Use sighting audits when:

- Assets are mobile, so teams need a more flexible way to verify them.

- When assets are located in remote areas, full physical audits become difficult.

- If assets are spread across many small sites, a targeted approach improves coverage.

What controls make fixed asset audits easier?

Teams often ask how to make the next fixed asset audit faster. The answer is not “audit harder.” The answer is “control better.”

The strongest fixed asset audits sit on top of a few practical controls:

1. A clear capitalization and tagging trigger

When an item becomes a capital asset, the organization should know:

- Who creates the register record?

- When the asset gets tagged.

- Which fields must be completed before the asset is considered active?

2. A controlled transfer process

Assets move all the time. The weak point is rarely the move itself. The weak point is the missing update.

Require transfer workflows to capture:

- Capture both the “from” and “to” locations, along with the transfer date, so movement is clearly tracked.

- Record the custodian and approver details as well, ensuring accountability at each step.

- Also, update any changes in cost center or department, so records remain accurate and aligned.

3. Monthly FAR-to-GL reconciliation

Do not wait for the annual count to discover that the fixed asset register and general ledger disagree.

A monthly reconciliation helps finance catch:

- Additions posted to the GL but not to the register.

- The register activity was not posted correctly to the GL.

- Retired assets that still carry depreciation.

4. Controlled disposal and write-off workflow

Disposals need stronger discipline than many companies realize.

A good disposal control includes:

- Start with a formal disposal request, so every action is properly initiated.

- Follow this with a clear approval process, ensuring the right authority signs off.

- Capture supporting evidence as well, whether it is a sale, scrap, transfer, or loss.

- Review the accounting entries carefully, so financial records stay accurate.

- Finally, close the asset in the register, ensuring the disposal is fully completed.

5. Periodic physical verification

Even strong systems drift over time. Regular physical verification keeps movement, misuse, and stale records from accumulating.

6. Exception management

Every audit produces exceptions. Mature teams track them in a formal log with:

- Assign a clear owner for each exception, ensuring someone takes responsibility.

- Identify the root cause, so you address the issue at its source.

- Define the required action clearly, so teams know exactly what to do next.

- Set a due date, so teams close issues on time.

- Capture closure evidence, so you can verify that the issue is fully resolved.

Common findings and how to fix them

The same fixed asset audit findings appear again and again. The fastest way to improve the next cycle is to classify them correctly and assign the right fix.

Finding |

What it usually means |

Likely root cause |

Best next action |

|---|---|---|---|

| Asset on books but not found | Possible ghost asset or bad location data | Missing transfer, unrecorded disposal, poor prior audit | Recheck last known site, review transfer/disposal records, escalate for write-off if unresolved |

| Asset found but not in register | Unrecorded asset or capitalization gap | Manual procurement workarounds, incomplete project closeout | Validate ownership and cost support, create or correct register entry |

| Wrong location or custodian | Control weakness, not always accounting error | Informal movement process | Update records and tighten transfer workflow |

| Wrong asset class or description | Reporting and depreciation risk | Weak master data governance | Correct class, useful life, and reporting mapping |

| Disposed asset still active | Overstated asset base and depreciation error | Disposal not posted end-to-end | Derecognize, reverse depreciation where required, and review approval flow |

| Idle or damaged asset still active | Potential impairment or utilization issue | Weak maintenance and review signals | Flag for finance and operations review |

| Duplicate asset records | Overstatement risk | Migration error, duplicate tagging, and manual imports | Merge records after validation and clean master data |

The failure mode most teams underestimate

The most underestimated failure mode is the cross-system mismatch.

>For example:

- Finance tracks an asset in the fixed asset register.

- IT tracks the same item in ITAM or CMDB.

- Operations track it by a local serial or plant number.

- Nobody owns the cross-reference.

That is how assets become “visible” in three systems and reliable in none.

What should the final report include?

Many fixed asset audit reports stop at exception counts. That is not enough for finance leadership, internal audit, or external auditors.

>A strong final report should include the following sections.

1. Executive summary

State:

- Why was the audit performed?

- What population was covered?

- What coverage rate was achieved?

- What is the overall conclusion?

2. Scope and methodology

Explain:

- Asset classes.

- Locations.

- Time period.

- Method used.

- Exclusions.

- Evidence standards.

3. Coverage statistics

Show:

- Total population.

- Verified count.

- Unverified count.

- Exceptions by class.

- Unresolved items.

4. Exception analysis

Group exceptions by type:

- Missing assets.

- Unrecorded assets.

- Data errors.

- Wrong location.

- Disposal issues.

- Control failures.

5. Financial impact

Where material, estimate the likely impact on:

- Gross block.

- Accumulated depreciation.

- Net book value.

- Write-off.,

- Impairment review.

6. Control observations

Separate control weaknesses from pure data errors. This helps internal audit and management prioritize durable fixes.

7. Remediation tracker

For each material issue, assign:

- Assign an owner, so someone takes responsibility.

- Define the action, so the owner knows what to do.

- Set a due date, so teams close issues on time.

- Track closure status, so you ensure completion.

A simple reporting framework by audience

| Audience | What they care about most |

|---|---|

| CFO / Controller | Financial impact, close confidence, recurring issues |

| Internal Audit | Control weakness, root cause, evidence sufficiency |

| Asset Manager | Missing assets, movement discipline, tagging quality |

| Operations Leader | Downtime, idle assets, and branch-level accountability |

| External Auditor | Reliability of evidence, completeness of reconciliations, treatment of discrepancies |

Country-specific guidance for the USA, India, and the UK

USA: Fixed asset audit as ICFR support

For US issuers and SOX-scoped environments, a fixed asset audit should support internal control over financial reporting, not sit outside it. That means the audit should do more than prove existence. It should also support:

- Maintain accurate records of additions, transfers, and disposals, so financial data stays reliable.

- Detect unauthorized use or disposal in time, so teams can act quickly.

- Reconcile the asset register with reported balances, ensuring consistency in financial reporting.

In practical terms, US finance teams should keep an evidence pack that links field verification to:

- Link field verification to the fixed asset register, so records stay aligned.

- Connect it to the GL reconciliation as well, ensuring financial consistency.

- Include approvals, so you maintain control and accountability.

- Track exception resolution, so you close issues properly.

India: Fixed asset audit as CARO-ready documentation

In Indian companies, physical verification of PPE is not just a process preference. It directly affects how auditors report under CARO 2020. That is why Indian finance teams should document:

- What was verified?

- How often is it verified?

- What discrepancies were found?

- How were they evaluated?

- How were they dealt with in the books?

For large or geographically dispersed organizations, a phased verification program can still work. However, it needs a defendable rationale, consistent documentation, and visible closure of discrepancies.

UK: Fixed asset evidence as part of material-control review

UK organizations, especially those with board-level governance expectations, increasingly rely on fixed asset evidence beyond finance. A mature fixed asset audit helps management show that controls over capital assets actually operate in practice:

- Asset records are maintained.

- Movements are tracked.

- Disposals are approved.

- Material controls are reviewed with evidence, not assumptions.

For UK finance teams reporting under FRS 102, that evidence also helps support cleaner PPE accounting and a more confident review of depreciation and impairment-related data.

How software changes the audit workflow

Spreadsheets can help with planning. They rarely help with evidence discipline at scale. A software-led workflow changes the fixed asset audit in five practical ways:

1. It starts with a cleaner data import

Instead of rebuilding lists manually, teams can import the asset register from ERP, CMDB, or existing files and assign work from a common starting point.

2. It gives field teams guided verification

Auditors or site teams can scan tags, capture photos, confirm condition, and update location or custodian details in one workflow instead of juggling paper sheets and follow-up emails.

3. It centralizes discrepancy handling

Supervisors can review missing, moved, duplicate, or unrecorded assets in a structured queue rather than piecing together comments from multiple spreadsheets.

4. It improves audit trail quality

When every field action is timestamped and linked to the user, location, and proof, teams build a defensible evidence pack with clear accountability and audit-ready support.

5. It closes the loop into the finance systems

The best outcome is not just a report. The best outcome is an updated and reconciled register that can flow back into ERP and reporting systems.

AssetCues’ asset verification software is designed around that operating model. It supports import from ERP or CMDB, task assignment to field teams, mobile verification with scans, photos, and geolocation, discrepancy review, and sync back to systems such as SAP, Oracle, or Dynamics. It also highlights tamper-proof audit logs and support for barcodes, RFID, and IoT-enabled tracking.

Key takeaways

- A fixed asset audit is not just a physical count; it is, instead, a combined review of existence, record accuracy, accounting treatment, controls, and reporting.

- The fastest way to improve audit outcomes is to build an evidence stack that clearly connects field proof with finance and control proof.

- Good fixed asset audits test both directions—books to floor and floor to books—at the same time, ensuring complete coverage.

- The right audit method depends on asset mobility, scale, control maturity, and site complexity; moreover, these factors shape the level of testing required.

- The final report should quantify findings, separate control weaknesses from data errors, and, in turn, assign clear remediation owners.

- The strongest teams treat fixed asset audit as a year-round process, ultimately avoiding a last-minute, year-end scramble.

Conclusion

A strong fixed asset audit is not a one-time exercise; it is a structured control process that connects physical assets, the fixed asset register, and financial records. When teams clearly define scope, apply consistent verification methods, and maintain proper documentation, the audit becomes easier to manage and far less disruptive. As a result, teams identify discrepancies earlier, improve accountability, and produce more reliable reporting across finance, audit, and operations.

In addition, organisations that treat fixed asset auditing as a continuous discipline—supported by clear controls and well-documented evidence—reduce last-minute corrections and avoid recurring findings. With the right workflow and supporting software, fixed asset audits can move from reactive cleanups to a predictable, repeatable process that strengthens compliance, supports accurate depreciation, and builds long-term confidence in asset data.

Frequently asked questions

Q1: What is the difference between a fixed asset audit and a fixed asset verification?

Ans: Fixed asset verification usually focuses on confirming the physical existence, location, and condition of assets. A fixed asset audit is broader. It includes verification, register accuracy, depreciation and disposal checks, approvals, and control evidence.

Q2: What documents do auditors usually ask for during a fixed asset audit?

Ans: Auditors usually ask for the fixed asset register, GL reconciliation, capitalization support, invoices, transfer records, disposal approvals, depreciation reports, and evidence from physical verification. The exact pack varies by scope and audit type.

Q3: What happens when an asset is missing during an audit?

Ans: When an asset is missing, the team should first recheck the last known location, custodian, and movement history. If the asset remains unresolved, the issue should move into the exception log and, where necessary, into disposal, write-off, or investigation workflow.

Q4: How does a fixed asset audit affect depreciation?

Ans: A fixed asset audit can identify incorrect in-service dates, useful lives, asset classifications, disposals, and idle or impaired assets. As a result, these findings may require adjustments to depreciation expense and net book value. In turn, this ensures more accurate financial reporting, compliance with accounting standards, and better alignment between physical assets and financial records.

Q5: Should IT assets be included in a fixed asset audit?

Ans: Yes, organizations should include IT assets when they capitalize them or when they remain relevant to the asset register. In practice, laptops, servers, network hardware, and user-assigned devices often need reconciliation across finance, ITAM, and CMDB records.

Q6: What is the difference between wall-to-wall and file-to-floor?

Ans: Wall-to-wall means verifying the entire physical asset population in a location or scope. File-to-floor starts with the asset register and checks whether listed assets can be found physically. Each method answers a different risk question.