Introduction

Disposals are where fixed asset records most often break: the laptop leaves the building or the machine is scrapped, but the register still says “active”, and depreciation keeps running. In an enterprise that creates audit findings, “ghost assets,” and real security exposure for data-bearing devices. Effective fixed asset management practices help prevent these issues by ensuring assets are properly tracked throughout their lifecycle, including disposal. This guide explains how fixed asset disposal accounting and IAS 16 derecognition rules help organizations correctly dispose of or write off fixed assets through a disposal workflow you can prove—approvals, evidence packs, journal entries, and reconciliation.

In this guide, you’ll learn:

- What fixed asset disposal accounting and derecognition mean under IAS 16, and why accurate removal of retired assets is essential for reliable financial reporting.

- Why strong disposal controls and documentation matter, especially to prevent audit issues such as ghost assets, incorrect depreciation, or missing approvals.

- How to build an auditable fixed asset disposal workflow, including approvals, evidence packs, segregation of duties, and reconciliation with the asset register.

- How to handle specialized cases like IT asset disposal, where data sanitization, chain-of-custody records, and security compliance are critical.

What is fixed asset disposal accounting, and what does “derecognition” mean?

Fixed asset disposal accounting refers to the steps organizations take to remove a long-term asset from their books when they sell, scrap, donate, lose, or otherwise retire it. “Derecognition” is the accounting term for this removal: IAS 16 requires derecognition on disposal or when no future economic benefits are expected from use or disposal.

In practice, derecognition is not “just a journal entry.” It is a point where three truths must align:

- Physical truth: the asset is actually gone/unusable (custody and location reality).

- Financial truth: the carrying amount and proceeds are captured correctly at the right time.

- Governance truth: You can prove approvals and supporting documentation exist for the scenario.

Disposal vs write-off (the practical difference)

In enterprise workflows, the words get used loosely, but the control design is easier when you separate them:

- A disposal often refers to an asset leaving custody via sale/donation/recycling, so evidence centres on transfer/handover documents.

- A write‑off is frequently triggered by “no future economic benefits,” including missing/stolen/destroyed assets, so evidence includes incident investigation and management authorization before derecognition.

Which disposal scenarios need different evidence?

Most disposal scenarios share the same accounting destination—derecognition—, but they need different evidence to prove what happened and when. IAS 16 itself notes disposals can occur in various ways, including sale and donation, and links disposal timing to when control transfers (important for cut-off).

Disposal scenarios and evidence pack checklist

Scenario |

Typical trigger |

Minimum evidence pack (examples) |

Common control risk |

|---|---|---|---|

| Sale | Sold to a third party | Approved disposal request; sales contract/invoice; proof of receipt; handover note; tag + serial verification; journal posting reference | Cut-off errors, wrong proceeds or fees, and missing approval |

| Scrap/retirement | Unusable, scrapped | Approved scrapping memo; recycler certificate (or internal scrap record); photos (where practical); tag retirement/destruction record | The asset was scrapped physically, but is still depreciating |

| Donation | Donated to charity/school | Approval; donation letter/acknowledgement; handover note; tag + serial verification | Missing proof of transfer; policy breaches |

| Loss/theft/damage | Missing/stolen/destroyed | Incident report; investigation notes; management approval to write off; police report/insurance claim, where applicable | Writing off without sufficient investigation |

| Abandonment / “no future benefit” | Retired with no expected benefit | Retirement memo; condition assessment; approvals; verification notes | Confusing “temporarily out of use” with abandonment |

Why these documents matter: IAS 16’s derecognition trigger (disposal or no future benefits) is easy to state, but an auditor will still ask for observable support that the trigger is real, and that it happened in the period you recorded it.

What does IAS 16 require at derecognition, and where does IFRS 5 fit?

For IFRS reporters, IAS 16 is the anchor: derecognise PPE on disposal or when no future economic benefits are expected. Organizations recognise the gain or loss in profit or loss when they derecognise the asset, and they do not classify such gains as revenue under the normal derecognition model. The gain/loss is the difference between net disposal proceeds and carrying amount.

→ Gain/loss calculation and presentation (the part that must be consistent)

At a high level, the mechanics are:

- Determine carrying amount at the derecognition date (cost less accumulated depreciation/impairment, or revalued carrying amount if using revaluation model).

- Determine net proceeds (if any).

- Gain/loss = net proceeds − carrying amount.

- Recognise gain/loss in profit or loss; do not classify gains as revenue (subject to specific exceptions described below).

→ Disposal date and cut-off

IAS 16 ties the disposal date to the point at which the recipient obtains control, referencing the IFRS 15 concept of control transfer for timing. For the month-end close, this is the difference between “we signed something” and “the transfer actually happened.”

→ Component replacement derecognition (often missed in operational SOPs)

IAS 16 states that if you recognise the cost of a replacement for part of an asset, you derecognise the carrying amount of the replaced part—even if it wasn’t separately depreciated. If it’s impracticable to determine that carrying amount, replacement cost can be used as an indicator of the replaced part’s cost at acquisition/construction.

→ A key IAS 16 nuance—rental assets routinely sold

IAS 16 also covers a specific scenario. When an entity routinely sells items it previously held for rental, it transfers those items to inventories at their carrying amount once they stop being rented and become held for sale. The entity then recognises the sale proceeds as revenue under IFRS 15, and IFRS 5 does not apply to these inventory transfers. Although this situation is not a typical fixed asset disposal case, it can create confusion if organizations do not clearly define their policies.

→ Where IFRS 5 changes the pathway (held for sale)

If an asset is classified as held for sale, IFRS 5 requires measurement at the lower of carrying amount and fair value less costs to sell, and it requires that you do not depreciate the asset while it is classified as held for sale. This is a different state than “disposed”; it affects how you support valuation and timing before the sale closes.

If you apply the revaluation model, practitioner summaries commonly note that revaluation surplus related to a disposed asset remains in equity (not reclassified to profit or loss), with potential transfer within equity depending on policy.

How do you build an auditable fixed asset disposal SOP?

An auditable disposal SOP is a workflow designed so a reviewer can trace: asset identity → approvals → scenario documents → carrying amount and gain/loss working → posting → register status change → reconciliation. IAS 16 gives the accounting trigger and gain/loss logic, but your SOP supplies the evidence and control design that makes it audit-ready.

Below is an enterprise-ready SOP you can standardise across regions and asset classes.

An auditable fixed asset disposal SOP ensures that every disposal or write-off is properly documented—from asset verification and approvals to journal entries and reconciliation. By following a structured workflow aligned with IAS 16 derecognition rules, organizations can create clear evidence, maintain strong controls, and stay audit-ready.

Disposal SOP (approvals + evidence + audit trail)

1) Trigger and classify the event

Classify the scenario (sale/scrap/donation/loss/theft/retirement). Decide whether it is (a) immediate derecognition or (b) a held-for-sale classification. If it’s IT equipment, flag it as a security event.

2) Verify identity (prevent “wrong asset” write-offs)

Verify tag + serial against the register record (description, location, custodian). Capture a timestamped verification (scan log, photo, signed handover). If the asset cannot be located, treat it as a missing-asset incident, not a routine disposal.

3) Confirm depreciation up to the right date

Ensure teams post depreciation up to the disposal date (or up to the held-for-sale classification date if IFRS 5 applies, since depreciation stops once the asset is classified as held for sale).

4) Approvals and segregation of duties

Design approvals so that one person cannot request, approve, and post the disposal. A common enterprise pattern: – Business owner/custodian confirms physical retirement/handover.

- Finance validates derecognition treatment and numbers.

- IT/security validates sanitization for data-bearing assets.

- Controller approves final derecognition above thresholds.

5) Assemble the evidence pack (make audit self-serve)

At minimum, build a pack that supports common assertions (existence, completeness, valuation, rights/obligations):

- Disposal request and approvals (role + name + timestamps)

- Asset record snapshot (tag, serial, description, acquisition date, location, custodian)

- Scenario documentation (invoice/contract; scrap certificate; donation acknowledgement; incident reports)

- Carrying amount calculation at disposal date and gain/loss working (net proceeds vs carrying amount)

- Journal entry and posting reference (FA subledger + GL)

- Register status update record (e.g., “disposed”, “scrapped”, “written off”)

- Reconciliation proof (disposal list reconciled to the GL)

6) Post derecognition and lock the record

Prefer disposals posted via a fixed asset subledger so the asset’s status changes and depreciation stops by design. Lock disposed assets against further edits/transfers unless via controlled adjustment workflow.

7) Reconcile and run exception reporting

At close, reconcile disposals: register disposals vs subledger disposals vs GL postings. Explicitly report: – Physically disposed assets still active in records (ghost assets)

- Derecognised assets still appearing in counts

- Missing approvals/evidence packs

- Late postings affecting period cut-off

8) Retain and audit-proof the trail

Store evidence packs in a governed repository (consistent naming, retention, access controls). For IT assets, retain sanitization certificates and chain-of-custody documentation as part of the same pack.

How do IT assets change the disposal workflow?

For laptops, servers, phones, and storage media, disposal is both an accounting derecognition event and a data security event. Media sanitization guidance (NIST SP 800‑88 Rev. 1) frames sanitization as making access to target data infeasible for a given effort level, and it includes a sample certificate (Appendix G) to document sanitization activities.

IT disposal: the minimum evidence you should be able to produce

- Device identity: tag + serial number (and drive serials, where feasible)

- Sanitization method used (aligned to your policy and risk classification)

- When and by whom was sanitization performed

- Chain-of-custody: handover points, transport logs, vendor receipt

- Certificate of sanitization/destruction listing serial numbers (internal or vendor-issued)

If you use third-party ITAD vendors, include serial-level certificates and custody records as contractual requirements. If you rely on remote wipe for encrypted endpoints, define in your policy when it is acceptable and how teams must document it, since auditability matters as much as the technical step.

What are common journal entries for fixed asset disposals?

The accounting pattern for disposal is consistent under IAS 16: remove the asset’s carrying amount from the books, recognise proceeds if any, and recognise the resulting gain or loss in profit or loss (with gains not classified as revenue in the standard derecognition model). Your exact accounts vary, but the evidence linking the entry to the asset record should not.

Example journal entries (non-software-specific)

Example: Sale at a gain

– Cost: $54,000

– Accumulated depreciation to disposal date: $45,360

– Carrying amount: $8,640

– Net sale proceeds: $10,800

– Gain: $2,160 (10,800 − 8,6400)

Journal (simplified):

– Dr Cash/Bank $10,800

– Dr Accumulated depreciation $45,360

– Cr PPE – cost $54,000

– Cr Gain on disposal (P&L) $2,160

Example: Scrap with zero proceeds

– Cost: $21,600

– Accumulated depreciation: $16,200

– Carrying amount: $5,400

– Proceeds: $0

– Loss: $5,400

Journal (simplified):

– Dr Accumulated depreciation $16,200

– Dr Loss on disposal (P&L) $5,400

– Cr PPE – cost $21,600

Example: Write-off after theft + later insurance recovery

IAS 16 requires organizations to remove an asset when it no longer expects future economic benefits. Organizations must document insurance recoveries separately and account for them consistently with internal policies and the relevant guidance.

At write-off date (simplified): – Dr Loss on disposal (P&L) $15,240

– Cr PPE (derecognition) $15,240

When insurance proceeds are received later: – Dr Cash/Bank $8,890

– Cr Insurance recovery / other income $8,890

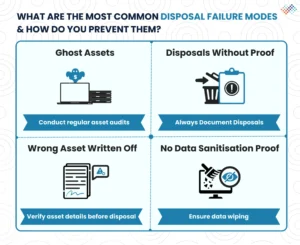

What are the most common disposal failure modes, and how do you prevent them?

Most disposal problems recur in the same places: weak identity controls, weak approvals, weak evidence retention, and weak reconciliation. IAS 16 states the derecognition outcome; your controls determine whether you can prove the derecognition trigger and amounts in an audit.

Common failure modes and remediation playbook:

-

Ghost assets (physically gone, still active in records)

Fix: make status change mandatory at handover/scrap; system-lock depreciation when status becomes disposed; reconcile disposal lists every close.

-

Disposals posted without proof (audit exceptions)

Fix: evidence-pack completeness gate before posting; central repository linked to the asset ID.

-

Wrong asset written off (tag/serial mismatch)

Fix: require tag + serial verification at disposal; second-person review for high-value classes.

-

IT assets leave without sanitization evidence (security exposure)

Fix: chain-of-custody + certificate mandatory; missing proof treated as a security incident; use a standard certificate form structure (NIST Appendix G provides a model).

Key takeaways

- Derecognise PPE when it’s disposed of or when no future economic benefits are expected.

- The disposal gain/loss is net proceeds minus carrying amount, recognised in profit or loss; gains are not classified as revenue in the normal IAS 16 derecognition model.

- Treat disposal as a controlled process: verify identity → approve → collect evidence → post → reconcile → retain an evidence pack.

- For IT assets, disposal is also a security event: follow a sanitization standard and keep chain-of-custody + certificates.

Conclusion

Fixed asset disposal accounting becomes easy to audit when you design disposal as a workflow that produces evidence by default: verified identity, scenario-specific approvals, a complete evidence pack, clean derecognition entries, and tight reconciliation back to the GL. For IT assets, add sanitization proof and chain-of-custody so disposal is safe for both your financial statements and your security posture.

FAQ: Fixed asset disposal accounting

Q1. When do you derecognise a fixed asset under IAS 16?

Ans. You derecognise PPE on disposal, or when no future economic benefits are expected from its use or disposal.

Q2. Where does the gain or loss on disposal go?

Ans. According to IAS 16, organizations must recognise any gain or loss arising from derecognition in profit or loss when the asset is derecognised, and the standard specifies that these gains should not be classified as revenue under the normal derecognition model.

Q3. How do you calculate gain or loss on disposal?

Ans. IAS 16 determines gain/loss as the difference between net disposal proceeds (if any) and the carrying amount of the item at derecognition.

Q4. What changes if an asset is classified as held for sale?

Ans. IFRS 5 measures held-for-sale assets at the lower of carrying amount and fair value less costs to sell, and it says you do not depreciate assets while classified as held for sale.

Q5. What evidence should we retain for disposal to satisfy audit trail expectations?

Ans. At minimum: approvals, proof of the disposal scenario (invoice/scrap certificate/donation letter/incident report), carrying amount and gain/loss working, the journal entry, a register status update, and a reconciliation back to the GL. The accounting trigger and gain/loss model come from IAS 16; the rest is the operational proof that the trigger occurred.

Q6. How do IT assets change disposal requirements?

Ans. In addition to derecognition, you need sanitization and custody evidence. NIST SP 800‑88 Rev. 1 provides sanitization guidance and includes a sample certificate form to document sanitization activities.