Ownership verification is a cornerstone of effective asset management and audit practices for Property, Plant, and Equipment (PP&E). The ICAI Guidance Note on Audit of PP&E provides essential clauses to ensure that ownership rights are clearly established, documented, and verified. This article focuses exclusively on ownership verification, examining the relevant clauses and their implications.

Key Clauses for Ownership Verification

Clause 42: Reliable Measurement and Economic Benefit

This clause mandates that the cost of a PP&E item should be recognized as an asset only when it can be reliably measured and future economic benefits are assured.

Explanation:

For ownership verification, this implies the auditor must confirm that the recorded costs relate to assets genuinely owned by the entity. For instance, invoices, purchase agreements, or contracts should clearly state the entity as the rightful owner. If an asset is acquired under lease or other arrangements, proper classification under ownership laws is critical.

Clause 43: Compliance with Accounting Standards

This clause emphasizes that ownership recognition must align with generally accepted accounting principles (GAAP) applicable to the entity.

Explanation:

Ownership records must be corroborated by legally binding documentation, such as title deeds for land and buildings or ownership certificates for vehicles. This ensures that only assets legally owned by the entity are recorded in its financial statements.

For example, an organization claiming ownership of a property must provide evidence, such as registered sale deeds or tax receipts, to demonstrate its legal title.

Clause 44: Capital Work in Progress (CWIP)

Ownership verification extends to assets classified as Capital Work in Progress. Clause 44 requires that only legitimate costs directly attributable to the asset under construction be included in CWIP until it is ready for intended use.

Explanation:

Auditors must verify that ownership of assets under CWIP is established through contracts, invoices, and legal agreements. For instance, if a company is constructing a manufacturing plant, the auditor should confirm that land acquisition and construction contracts are registered under the entity’s name, ensuring no ambiguity in ownership rights.

Clause 45: Component Approach and Ownership

Under the component approach, Clause 45 directs that significant parts of an asset with varying useful lives must be separately accounted for. Ownership of each component must also be validated.

Explanation:

For example, an aircraft’s engine and fuselage, being separate components, may have distinct ownership documents if acquired from different vendors. The auditor must verify the purchase agreements, delivery receipts, and vendor certifications to establish ownership for each major component.

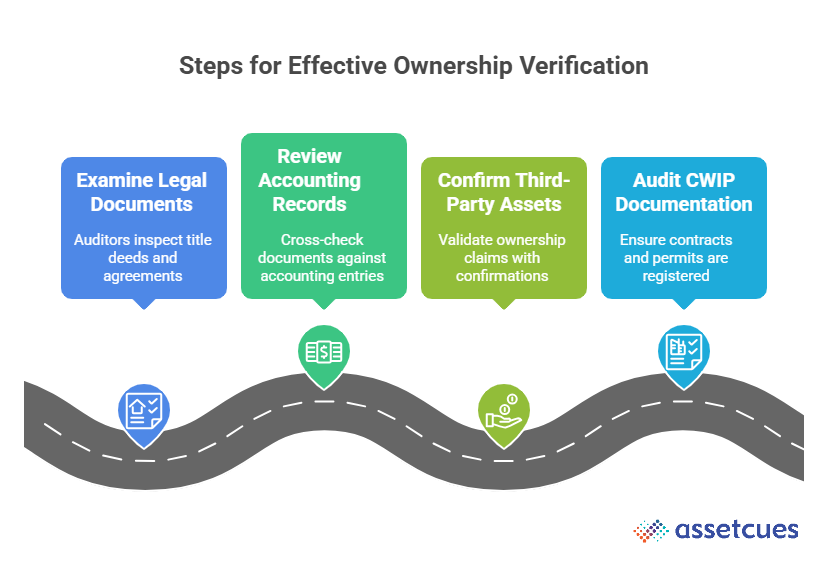

Steps for Effective Ownership Verification

-

Examine Legal Documents:

- Auditors should inspect title deeds, purchase agreements, vendor invoices, and registration certificates to ensure the entity holds valid ownership rights.

-

Review Accounting Records:

- Cross-check ownership documentation against accounting entries to verify consistency in records and proper asset classification.

-

Confirm Third-Party Assets:

- For assets held by third parties, auditors should obtain confirmations or inspect lease and custody agreements to validate ownership claims.

-

Audit CWIP Documentation:

- Ensure that contracts, permits, and invoices related to assets under construction are registered in the entity’s name to prevent disputes over ownership.

Conclusion: Ownership Verification as a Pillar of Accountability

Ownership verification of PP&E, as outlined in the ICAI Guidance Note, ensures that only assets genuinely owned by the entity are reflected in financial records. By adhering to the relevant clauses, management and auditors can establish a transparent and defensible framework for asset ownership, enhancing the integrity and reliability of financial reporting.

Would you like further refinements or examples to enhance this version?