Introduction

Confused about whether asset reconciliation means a physical check, a register clean-up, or a finance control? This guide defines the term, separates it from asset verification, and shows which deeper guide to use next.

Asset reconciliation is the process of comparing asset records with physical assets or supporting financial records, identifying mismatches, investigating the cause, and updating the records so that the data is accurate, current, and auditable. A deeper look at how reconciliation in asset management works across fixed asset registers, subledgers, and physical counts helps clarify exactly where and how each of these steps plays out in practice.

In this guide, you’ll learn:

- What asset reconciliation actually means in practice, and how it connects records, physical assets, and financial data.

- How asset reconciliation differs from asset verification, and why both are needed but should not be treated as the same activity.

- Where fixed asset reconciliation fits within the broader concept, especially from a finance and audit perspective.

- The main types of asset reconciliation, along with when each type is used and what kind of mismatches it typically uncovers.

- Finally, what a practical asset reconciliation process looks like, including how teams investigate differences, correct records, and maintain a clear audit trail.

TL;DR

- Asset reconciliation means comparing, investigating, correcting, and documenting.

- Asset verification confirms existence, location, and condition.

- Fixed asset reconciliation is a narrower finance-and-audit subtype of asset reconciliation.

- Inventory reconciliation is different because inventory is held for sale or consumption, not long-term use.

What does asset reconciliation mean?

Asset reconciliation means bringing asset data back into agreement with reality. Depending on the scope, that reality may be the physical asset, the asset register, the fixed asset register, the general ledger, or another system of record. The underlying job stays the same: compare the record, explain the mismatch, and fix it.

The AssetCues record-to-reality ladder

Teams often blur four related activities together. In practice, they are different:

Activity |

Main question |

Typical output |

|---|---|---|

| Asset count | How many items did we find? | Count the sheet or scan the total |

| Asset verification | Did we find the right asset in the right place and condition? | Serial match, photo, timestamp, condition note |

| Asset reconciliation | Why does the record not match what we found or what finance posted? | Exception log, root-cause note, approved correction |

| Control improvement | How do we stop the same issue from repeating? | Policy change, workflow update, system automation |

Verification finds facts. Reconciliation turns those facts into corrected records.

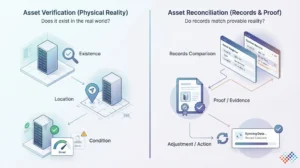

Is asset reconciliation the same as asset verification?

No. Asset verification answers the physical question: Does the asset exist, where is it, and what condition is it in?

Asset reconciliation answers the records question: Do the records match what the business can prove, and what must change if they do not?

Asset Reconciliation vs Related Terms

Term |

What it answers |

Typical output |

Primary owner |

|---|---|---|---|

| Asset verification | Does the physical asset exist in the recorded location and condition? | Verified list, field evidence, exception list | Ops, IT, facilities, field audit team |

| Asset reconciliation | Do the records match physical or financial reality, and how should we correct them? | Corrected records, approvals, and audit trail | Finance, asset managers, cross-functional owners |

| Fixed asset reconciliation | Do the fixed asset register, supporting evidence, and often the GL align for capitalized assets? | Tie-out, reviewer file, approved adjustments | Finance and audit |

| Inventory reconciliation | Do stock records match items held for sale or consumption? | Inventory variance report | Supply chain, warehouse, finance |

| Register clean-up | Is the master record complete and standardized? | Cleaned register | Asset admin, finance, IT |

Where fixed asset reconciliation fits

Fixed asset reconciliation is a subset of asset reconciliation, not a synonym for the broader term. It focuses specifically on capitalized assets, fixed asset register reconciliation, and key finance controls such as cost, accumulated depreciation, and disposal accuracy.

What are the main types of asset reconciliation?

Most businesses use the term in one of three ways:

Type |

What gets compared |

Typical use case |

Common mismatch |

|---|---|---|---|

| Physical asset reconciliation | Physical assets vs asset register | Branch checks, IT fleet reviews, and annual verification | Missing assets, wrong location, wrong custodian |

| Fixed asset register reconciliation | Fixed asset register vs supporting records and status | Audit prep, disposal cleanup, data hygiene | Unrecorded transfers, incomplete records, assets still shown as active |

| Ledger and depreciation reconciliation | Fixed asset register vs GL and depreciation records | Month-end close, year-end review, audit support | Missing additions, wrong useful life, unposted retirements |

In practice, one finding often triggers all three. Separating the types still helps teams assign the right owner and evidence.

Why do businesses perform asset reconciliation?

Businesses perform asset reconciliation because bad asset data slows close, weakens audit support, hides ownership issues, and turns simple disposals or transfers into control failures.

Why does each persona care?

Persona |

The main reason asset reconciliation matters |

|---|---|

| Finance | Supports close accuracy, capitalization, depreciation support, and disposal handling |

| Internal audit | Improves evidence quality, exception tracking, and control testing |

| IT / Ops | Keeps location, custodian, and movement history accurate |

| Asset managers | Makes the register usable and improves lifecycle visibility |

How the term shows up in the USA, India, and the UK

The phrase is broad, but the working context changes by country.

-

USA:

Finance teams often connect asset reconciliation to depreciation support and property records. IRS Publication 946 says businesses must keep records showing the business, investment, and personal use of depreciable property. Enterprise ERP documentation also uses the term in this finance sense; Oracle Assets Reconciliation Reports are designed to reconcile journal entries to general ledger accounts.

-

India:

Finance and audit teams often connect the term to PPE records, physical verification, and whether discrepancies are dealt with in the books. ICAI publishes guidance on CARO 2020 and audit of property, plant and equipment, which is why the phrase often carries stronger audit-readiness overtones in India.

-

United Kingdom:

Teams often connect the term to fixed asset records, capital allowances, and disposals. HMRC notes in its Capital Allowances Manual that accounting depreciation is not a tax deduction for taxable profits, and HMRC’s record-keeping guidance recommends keeping records of capital allowances claimed.

If the discussion becomes more accounting-specific, IAS 16 is the core standard for recognising property, plant and equipment and measuring carrying amounts, depreciation, and impairment.

What does a basic asset reconciliation process look like?

The basic flow is always the same: define the scope, compare the records, investigate the differences, correct the record, and preserve the evidence.

Asset reconciliation 6-step process

- Define the scope- Decide whether you are reconciling physical assets, fixed assets, IT assets, one site, or one asset class.

- Pull the current record set- Export the register, fixed asset register, or supporting ledger data with the key fields you need.

- Verify the real-world or financial position- Check physical assets on site, or review the supporting finance records, depending on the scope.

- Compare records against evidence- Flag missing, extra, duplicate, transferred, retired, or misclassified assets.

- Investigate the root cause- Determine whether the mismatch came from a transfer, disposal, onboarding gap, timing issue, or policy weakness.

- Update the record and preserve the trail- Correct the record, record the reason, secure approvals, and keep the evidence.

What does asset reconciliation look like in a real example?

1: The register and the site disagree

A company’s register lists 10 laptops for one branch.

- 8 laptops are found with the right employees.

- 1 laptop was transferred to another branch, but the register was never updated.

- 1 laptop was disposed of, but it still appears as active.

This creates three separate actions:

- Verification confirms what the team physically found.

- Reconciliation explains the transfer and disposal mismatch.

- Record maintenance updates the location and status fields, then attaches the supporting approvals.

2: Finance recorded an addition, but the register missed it

Observation |

Likely cause |

What reconciliation does |

|---|---|---|

| GL shows a new capitalized asset | Onboarding failed or was delayed | Trace the invoice, approval, and commissioning details |

| FAR is missing the record | The register update never happened | Create the asset record with the right class, cost, date, and location |

| Site team confirms the asset exists | Operational handoff happened without register creation | Attach field evidence and close the exception |

Reconciliation connects evidence to action.

Who usually owns asset reconciliation?

One team rarely owns every step. Ownership should follow the source of truth.

Scope |

Primary owner |

Supporting teams |

|---|---|---|

| Physical mismatch at a site | Ops, facilities, IT, asset manager | Finance, local custodian |

| Register data issue | Finance, asset admin | IT, ops, procurement |

| Capitalization or disposal issue | Finance controllership | Procurement, ops, audit |

| Audit exception | Finance and internal audit | Site owners, IT, ops |

The team closest to the evidence explains the mismatch, and the team responsible for the system of record approves the correction.

When do spreadsheets stop being enough?

Spreadsheets can work in small, stable environments. They struggle when asset movement, site count, or audit pressure rises.

Spreadsheets may be enough when |

Software becomes the better choice when |

|---|---|

| One team manages one site or a small asset base | The business runs multiple sites, entities, or departments |

| Asset movement is rare | assets move often between users, rooms, or locations |

| Audit evidence is simple and infrequent | The team needs photos, timestamps, mobile scans, and approval trails |

| Nobody needs real-time visibility | Finance and ops need one reliable source of truth |

Software becomes especially useful when the business needs to turn verification data into reconciliation-ready evidence quickly. If that is your use case, see asset reconciliation software.

Key Takeaways

- Asset reconciliation means bringing records back into agreement with reality.

- Asset verification and asset reconciliation are not the same activity.

- Fixed asset reconciliation is a subset of the broader term.

- Teams should define the scope before they start, because the word can point to physical, register, or financial work.

- A strong definition page should explain the term clearly and route the reader to the right next action.

Conclusion

Asset reconciliation brings clarity by aligning records with what the business can actually prove, whether through physical checks or financial support. While verification establishes the facts on the ground, reconciliation explains differences and ensures records are corrected with proper evidence and approvals. As a result, organizations gain more reliable data, smoother audits, and better control over asset lifecycle decisions.

")

Frequently asked questions.

Q1: What is the difference between asset reconciliation and fixed asset reconciliation?

Ans: Asset reconciliation is a broad term. More specifically, fixed asset reconciliation is the narrower finance-and-audit version that focuses on capitalized assets, the fixed asset register, and often the general ledger.

Q2: What is the difference between asset reconciliation and inventory reconciliation?

Ans: Inventory reconciliation deals with stock held for sale or consumption. In contrast, asset reconciliation deals with business assets used over time that need ownership, location, status, and sometimes valuation tracking.

Q3: Does asset reconciliation always require a physical count?

Ans: No. Some asset reconciliation work is finance-led and compares the fixed asset register to supporting records or ledger balances. However, physical verification becomes important when the business cannot trust the existence, location, or disposal status.

Q4: Can a company do asset reconciliation in Excel?

Ans: Yes, if the environment is small and stable. However, Excel becomes fragile when the business has multiple sites, frequent movement, or a need for evidence trails and approvals.

Q5: What is the output of a good asset reconciliation?

Ans: A good asset reconciliation produces a corrected record, a documented reason for each exception, along with the right approvals, and an evidence trail a reviewer can follow.

")