Introduction

Fixed asset verification matters when finance teams do not fully trust the asset register before close, audit, insurance renewal, ERP migration, or a multi-site clean-up. This guide explains what fixed asset verification and physical asset verification is, what it proves, how to run it, and how organizations can support the process using asset verification software to turn results into an audit-ready control process rather than a one-time count.

Verification of fixed assets is the management-led process of confirming that recorded property, plant, and equipment physically exists and that key record details, such as identifier, location, condition, and status, match reality. IAS 16 defines PPE as tangible items held for use and expected to be used during more than one period. Indian AS 10 uses the same basic framing, and ICAI’s CARO 2020 guidance makes clear that physical verification is a management responsibility that auditors later evaluate.

In this guide

- Understand what fixed asset verification involves and why it matters not just to finance, but also to audit and operations teams managing assets day to day.

- See how verification differs from processes like asset tagging, reconciliation, and valuation, which are often used interchangeably but serve very different purposes.

- Learn when companies typically run verification and how responsibility is usually shared between finance, IT, and operations.

- Walk through a practical, real-world approach to conducting fixed asset verification while keeping records accurate and audit-ready.

- Look at the discrepancies that most commonly appear during verification and how teams usually deal with them.

- Finally, explore what an audit-ready evidence pack should include, along with whether it makes sense to run verification in-house, use software, or bring in external specialists.

TL;DR

- Fixed asset verification confirms whether assets on the books actually exist and whether the register reflects real location, condition, and control status.

- Verification of assets is not the same thing as asset tagging, reconciliation, or valuation.

- A strong program follows six steps: baseline, scope, operating model, fieldwork, reconciliation, and closeout.

- Finance should own policy and reporting outcomes, but operations, IT, facilities, site custodians, and internal audit all play defined roles.

- Audit-ready verification needs more than a count sheet. It needs evidence, exception logic, approvals, and a clean handoff back into the register or ERP.

- In 2026, the winning version of this topic is control-led and country-aware, not just a longer how-to article.

What Is Fixed Asset Verification?

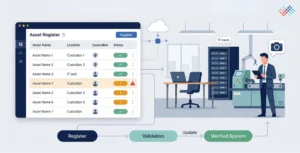

Fixed asset verification is the process of checking whether the fixed asset register matches on-ground reality. In practice, that means physically confirming an asset’s existence and then validating the record fields that matter for control and reporting: description, barcode or serial number, location, custodian, condition, status, and exception notes. For many enterprises, that process also includes photo evidence, geo-location, and structured discrepancy handling before approved changes flow back into ERP or CMMS records.

Why Finance, Audit, and Operations Care About Fixed Asset Verification

Finance cares because weak verification of assets leads to the wrong depreciation base, unresolved disposals, duplicate records, and year-end delays. Audit cares because verification of assets supports evidence over existence, accuracy, and the quality of management controls around PP&E. Operations, facilities, and plant teams care because location, usability, damage, and idle status affect maintenance planning, insurance, moves, and replacement decisions.

Globally, verification responsibilities differ:

- US: Supports management’s ICFR responsibilities.

- India: Aligns directly with CARO reporting requirements.

- UK: Provides evidence for annual control reviews.

- South Africa (public sector): Often requires location, condition, and audit-support deliverables.

What Fixed Asset Verification Is Not

A lot of weak content mixes four different activities together. They are related, but they are not interchangeable.

Activity |

Core question |

Typical output |

Why it matters |

|---|---|---|---|

| Asset tagging | How do we uniquely identify the asset? | Barcode, QR, RFID, BLE, or other physical identifier | Makes later verification faster and cleaner |

| Fixed asset verification | Does the recorded asset physically exist, and do key details match reality? | Verified field evidence plus exceptions | Supports control, audit, and operational accuracy |

| Reconciliation | How do we resolve differences between field results and the register? | Discrepancy log, approved adjustments, cleaned register | Converts findings into accounting and system corrections |

| Valuation/revaluation | Is the asset recorded at an appropriate carrying amount or fair value basis? | Valuation report, impairment or revaluation entries | Supports measurement, not physical existence |

Tagging makes verification easier. Verification generates the facts. Reconciliation resolves the mismatches. Valuation answers a different question about measurement. AssetCues’ own product and asset verification and tagging services separate these motions clearly: software focuses on capture, exception handling, audit logs, and ERP sync, while services emphasise baseline creation, annual verification, tagging, lender or insurer support, and valuation-ready field evidence.

What Does Fixed Asset Verification Actually Prove?

A useful verification program proves more than “we counted some assets.” It proves whether the register is dependable enough for reporting and control decisions.

Control objective matrix

Verification activity |

What it confirms |

Evidence captured |

Main risk reduced |

|---|---|---|---|

| Barcode / serial scan | Existence and identity | Tag or serial match | Ghost or duplicate assets |

| Location confirmation | Physical placement | Building, floor, room, plant, line, or branch | Wrong-site or wrong-cost-centre records |

| Custodian confirmation | Control and accountability | User/department/owner field | Orphaned or disputed ownership |

| Condition assessment | Usability and impairment signals | In use, idle, damaged, obsolete | Overstated carrying value or poor replacement planning |

| Floor-to-file check | Completeness of the register | Unrecorded additions found in the field | Missing capitalisation or off-book assets |

| File-to-floor check | Accuracy of existing records | Items selected from the register and traced physically | Assets on the books that cannot be found |

| Exception review | Resolution quality | Reason codes, approvals, and action owner | Findings that never get closed |

A balanced point matters here: physical verification supports evidence over existence, location, condition, and completeness indicators, but it does not replace legal-title checks, capitalisation review, disposal approvals, or valuation work. CARO guidance treats title deeds and proper records as separate matters, and that is the right way to think about enterprise controls, too.

When Should Companies Run Fixed Asset Verification?

The short answer is: before the business can no longer tolerate uncertainty in the register.

The most common triggers are year-end close, statutory audit preparation, multi-location register clean-up, ERP or CMMS migration, post-merger baseline creation, insurance review, lender requirements, or revaluation work. AssetCues’ services page explicitly positions verification for annual financial close, compliant financial reporting, lender and insurer requirements, and valuation or revaluation exercises.

The better question is not “annual or not?” but “what cadence does each set of assets deserve, and how should it be aligned?” Indian CARO reporting uses the phrase “reasonable intervals,” not “every asset every year.” UK control-review language focuses on material controls and the annual review of effectiveness. South African public-sector policies often go further and define annual, quarterly, or monthly routines for different asset groups. A well-defined fixed asset physical verification policy sets a risk-based cadence by mobility, value, fraud exposure, asset density, and audit sensitivity.

A practical risk-based cadence model

Asset segment |

Suggested cadence |

Why |

|---|---|---|

| High-value mobile IT, lab devices, tools, shared equipment | Quarterly or continuous spot checks | These assets move often and go missing faster |

| Plant and machinery in fixed locations | Annual or rolling 12-month cycle | High value, lower mobility, strong audit relevance |

| Branch/office equipment | Annual or 18-month rolling cycle | Moderate risk, moderate mobility |

| Furniture and low-risk fixtures | 18–36 months with spot checks | Lower risk if movement is controlled |

| Embedded, underground, or non-visible assets | Alternative control plus periodic review | Physical inspection may be impractical or incomplete |

| Intangible assets | Alternative non-physical control only | They are not physically verifiable |

This is a model, not a law. Your policy should tune it by asset class, movement frequency, site complexity, and control environment.

Who Should Own Fixed Asset Verification?

Management owns it. Auditors evaluate it.

ICAI’s CARO guidance states that physical verification of assets is management’s responsibility, not the auditor’s. In the US, SEC rules require management to establish and maintain adequate internal control over financial reporting and assess effectiveness at year-end. In the UK, the board is expected to monitor the internal control framework and review effectiveness at least annually. That makes fixed asset verification a management control process with audit consequences, not an audit-only exercise.

Recommended RACI

Role |

Primary responsibility |

|---|---|

| Finance/controllership | Own policy, thresholds, reporting outcomes, reconciliation approvals |

| Fixed asset accounting | Maintain register, depreciation mapping, exception treatment, and book updates |

| Operations/facilities/plant | Provide site access, location knowledge, condition input, and custodian accountability |

| IT asset management | Own laptops, servers, network gear, CMDB or ITAM alignment |

| Internal audit | Review design, test coverage, and challenge unresolved exceptions |

| External service provider | Execute fieldwork or tagging at scale where needed |

| CFO / finance leadership | Approve policy, escalation rules, and year-end sign-off |

How Do You Conduct Fixed Asset Verification? A 6-Step Process

A strong process starts long before the first scan. It begins with a clean baseline and ends only when approved corrections flow back into the register. This end-to-end physical asset verification process is also reflected in how AssetCues structures its software workflow: import the register, assign field tasks, capture on-site evidence, resolve discrepancies, and sync verified results back into the ERP system.

-

Build the baseline

Start with one working set of assets. First, pull the fixed asset register, depreciation schedule, site list, recent additions, disposals, transfer logs, and department or custodian mappings into one baseline file.

At this stage, mark obvious exception sets:

-

- Leased assets

- Third-party assets on site

- Embedded or underground assets

- Pooled low-value assets

- Assets under installation

- Intangible assets

Do not send field teams out with three different source files and no tie-back logic.

-

Define scope, rules, and exceptions

Document what is in scope and what is not. Decide the asset classes, value thresholds, sites, departments, and proof requirements. Also, define how you will treat non-taggable assets, damaged assets, missing tags, inactive items, and items found in the field that are missing from the books.

This is where you choose the control method:

-

- File-to-floor: Start from the register and trace to the asset.

- Floor-to-file: Start from what exists physically and trace back to the register.

Good programs do both.

-

Choose the operating model

Pick the model that fits your bandwidth and control maturity:

-

- In-house, when you have disciplined site teams and a manageable footprint.

- Software-led when you want repeatable workflows, audit logs, and ERP sync.

- Outsourced when you need large-scale field execution or a baseline rebuild.

- Hybrid when finance wants control of ownership, but field capacity is limited.

-

Run field verification

Field teams should capture more than a yes/no result. They should confirm the identifier, exact location, condition, custodian or department, and exception status. Where appropriate, they should capture photo proof, geolocation, and notes.

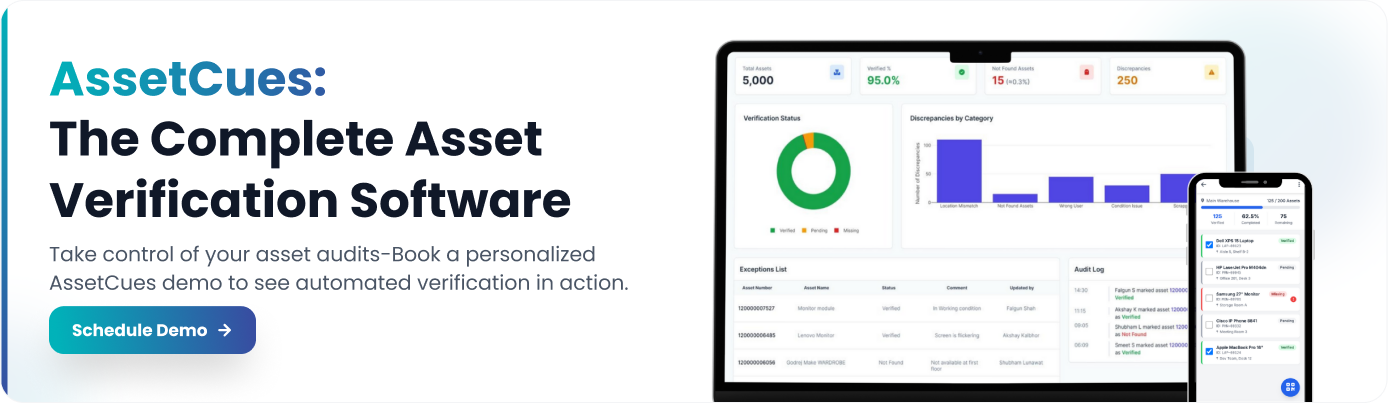

AssetCues’ product page highlights the right evidence pattern for 2026 programs: barcode or serial scans, photos, geolocation, exception handling, re-verification, audit logs, and ERP or CMDB connectivity. That is the model to benchmark against, even if you use a different platform.

-

Reconcile and classify discrepancies

Verification of assets is only half the job. Reconciliation turns field facts into accounting truth.

Create controlled discrepancy categories such as:

-

- Matched

- Wrong location

- Wrong custodian

- Unrecorded addition

- Not found

- Duplicate record

- Retired but still on books

- Damaged / obsolete/idle

- No tag / unreadable tag

Each category needs an owner, a resolution path, and a deadline.

-

Close the loop and issue the report

The cycle is not complete until approved changes return to the register, ERP, or CMMS. Close the process by preparing a comprehensive physical asset verification report that includes:

-

- Approved adjustments

- Updated records

- Final discrepancy log

- Management summary

- Action tracker

- Sign-off

That is what turns a field exercise into an audit-ready control.

What Discrepancies Show Up Most Often?

Most enterprises do not fail verification because assets vanish at scale. They fail because records drift slowly, and no one closes the gap.

Discrepancy |

What it usually means |

Common cause |

Action required |

|---|---|---|---|

| Asset not found | Book record has no confirmed physical match | Disposal not recorded, move not logged, tag loss, theft | Re-verify, investigate, approve write-off or further search |

| Wrong location | Asset exists, but not where the register says | Internal transfer, plant move, branch relocation | Update location and transfer controls |

| Wrong custodian | The asset is assigned to the wrong person or team | Joiner-mover-leaver gaps, handover failures | Update ownership and strengthen handoffs |

| Unrecorded addition | Asset exists in the field but not in the books | Capitalisation missed, local purchase, incomplete onboarding | Validate capitalisation and add to the register |

| Duplicate record | One asset appears twice in the system | Manual uploads, migration errors, tagging reset | Merge and correct history |

| Retired but still active in books | Asset no longer in use but remains capitalised | Disposal or retirement workflow failure | Process retirement or disposal |

| Damaged / obsolete/idle | Asset exists but does not support active use | Deferred disposal, no condition review | Assess impairment, replacement, or disposal |

| Untagged/unreadable tag | An asset cannot be identified reliably in the field | Tag wear, bad standards, no retagging rule | Re-tag with controlled governance |

South African public-sector verification specs are useful here because they explicitly require condition, location, useful life indicators, and reports on damaged, redundant, missing, or obsolete assets. That is a good reminder that a serious verification cycle should classify business conditions, not just physical presence.

What Should An Audit-Ready Evidence Pack Include?

An audit-ready evidence pack should let a reviewer answer three questions quickly:

- Which set of assets did management verify?

- What proof was captured?

- How were exceptions resolved?

ICAI’s CARO guidance stresses adequate evidence for management’s physical verification. SEC ICFR reporting centres management responsibility and effectiveness assessment. South African verification scopes often require explicit deliverables such as verification reports, location reports, damaged or missing asset reports, and trial-balance alignment support. Put differently, a count sheet alone is not enough.

Minimum contents of the evidence pack

- Approved scope, thresholds, exclusions, and timing.

- The set of asset files used for the cycle.

- Site coverage list.

- Verification instructions for field teams.

- Sample logic if you used one.

- Raw field evidence: identifier, location, condition, custodian, verifier, timestamp.

- Photos and geolocation were required.

- Discrepancy log with reason codes.

- Action tracker with owners and due dates.

- Management approvals for book changes.

- Final report and sign-off.

Finance lens

Finance should ask: Did the cycle produce a cleaner register, cleaner depreciation inputs, and fewer open exceptions at close?

Audit lens

Audit teams should ask: Is the set of assets clear? Is the proof traceable, and can each exception be followed to an approved outcome?

Operations lens

Operations should ask: Did the process improve asset visibility, condition awareness, and movement discipline?

Should You Run Verification In-House, Use Software, or Outsource It?

The right answer depends on scale, urgency, and internal maturity.

AssetCues’ fixed asset verification software is clearly built for recurring enterprise verification: import from ERP or CMDB, mobile field checks, photo and geo evidence, audit logs, multi-tech support, re-verification, and synchronised updates back into SAP, Oracle, or Dynamics, especially in environments where SAP asset verification plays a central role. Its services page is aimed at baseline creation, annual verification, large-scale tagging, compliant financial reporting, lender or insurer needs, and valuation support.

Model |

Best fit |

Main advantage |

Main risk |

|---|---|---|---|

| In-house | Limited sites, disciplined local teams, stable register | Lowest external cost, strong internal ownership | Often weak on speed and evidence consistency |

| Software-led | Recurring cycles, internal staff available, need audit logs and ERP sync | Scalable, repeatable, evidence-rich | Still requires process discipline |

| Outsourced | Many sites, tight deadlines, baseline rebuild, M&A, poor data quality | Fast field execution and specialist capacity | Can fail if ownership and handoff are weak |

| Hybrid | Finance wants governance, but field capacity is constrained | Best balance of control and execution | Needs a very clear RACI |

Software does not replace physical verification. Software improves planning, field capture, exception handling, and record synchronization. Someone still has to physically verify the fixed assets or apply an approved alternative control where physical inspection is impractical. South African public-sector specs make that distinction explicit by requiring physical verification for movable PPE while using alternative means for intangibles.

Country-Specific Audit Readiness Modules

USA: How fixed asset verification supports ICFR and external audit readiness

SEC rules require management’s annual internal control report to state management’s responsibility for establishing and maintaining adequate ICFR, identify the framework used for evaluation, and present management’s assessment of effectiveness as of fiscal year-end. Fixed asset verification, therefore, supports that control environment by producing evidence over the accuracy of the asset register, the closure of discrepancies, and the reliability of management’s supporting documentation. It does not, by itself, prove the whole control framework is effective, but it is a concrete piece of year-end control evidence.

◊What US finance teams should evidence

-

- Set of assets used for the cycle.

- Control the owner and reviewer.

- Evidence retained for exceptions.

- Approved book adjustments.

- Linkage to close and audit timelines.

India: What management should evidence for Companies Act / CARO-style questions

ICAI’s revised CARO 2020 guidance says auditors report whether the company maintains proper records showing full particulars, including quantitative details and the situation of PPE, whether PPE has been physically verified by management at reasonable intervals, and whether material discrepancies were properly dealt with in the books. That means Indian finance teams need more than a verbal assurance that a count happened. They need records, interval logic, discrepancy treatment, and a clean audit trail.

◊What India teams should evidence

-

- Asset records with location and identification detail.

- Policy language defining “reasonable intervals”.

- Field evidence tied back to the register.

- Discrepancy log with accounting treatment.

- Management sign-off before audit close.

United Kingdom: What UK finance teams should evidence for board-ready control reviews

The FRC says the 2024 UK Corporate Governance Code applies from financial years beginning on or after 1 January 2025, with Provision 29 applying from financial years beginning on or after 1 January 2026. Provision 29 requires the board to monitor the risk-management and internal-control framework and carry out at least an annual review of effectiveness, while the guidance explains that boards should make a declaration on the effectiveness of material controls at the balance-sheet date. Fixed asset verification supports that narrative when PP&E records, site governance, and asset-movement controls are material to reporting or operations.

◊What UK teams should evidence

-

- Why are fixed asset controls material?

- How were sites covered?

- What control failures or near-misses were found?

- What remediation happened before year-end?

- What evidence supported the board’s conclusion?

South Africa: What a South Africa-ready verification report should include

Current South African public-sector scopes and policies are unusually concrete about verification deliverables. For example, asset verification reports include description, location, and condition; location reports by office; and damaged, redundant, or missing asset reports. In addition, assistance with aligning the asset register to the trial balance, support for audit queries and PFMA/GRAP compliance, GIS-linked photographs as proof of existence, and scheduled annual, quarterly, or monthly verification routines depending on asset type. As a result, this makes South Africa a strong market for evidence-rich, report-heavy verification content.

◊What South African teams should evidence

-

- Location and condition at the asset level.

- Additionally, photographic or GIS-linked proof where relevant.

- Missing/damaged / obsolete schedules.

- Furthermore, useful-life or impairment indicators.

- Finally, register-to-trial-balance alignment support.

Common Failure Modes That Make Verification Weak

- Treating verification as a count, not a control.

If the cycle ends at counting, the register stays wrong. - Confusing tagging with verification.

A tag is an identifier, not proof that the record is accurate. - Skipping floor-to-file coverage.

That is how unrecorded additions survive for years. - Letting every site use different evidence standards.

Inconsistent proof destroys comparability and audit confidence. - Closing the fieldwork, but not the exceptions.

A discrepancy log without owners and deadlines is just a backlog. - Using software without governance.

Better tools help, but weak approvals still produce weak records. - Ignoring the exception set of assets.

Embedded, underground, leased, third-party, and intangible assets, therefore, need explicit alternate handling.

Key Takeaways

- Verification of assets confirms whether assets recorded in the register actually exist and whether key details like location, condition, and ownership match reality. As a result, it strengthens trust in financial and operational data.

- A strong verification process follows a structured approach—from preparing a clean baseline and conducting field checks to reconciling discrepancies and updating the asset register. Otherwise, verification remains incomplete.

- Most issues arise from record gaps rather than missing assets, such as wrong locations, unrecorded additions, or outdated ownership details. Therefore, resolving discrepancies is just as important as the physical check itself.

- Ultimately, fixed asset verification works best as an ongoing control process, not a one-time exercise, thereby ensuring audit readiness, accurate reporting, and better decision-making across finance and operations.

Conclusion

Fixed asset verification should not be treated as a once-a-year scramble. It should be a repeatable control that connects field evidence, discrepancy handling, reporting, and register accuracy. When teams design it that way, verification becomes useful to controllers, auditors, plant heads, facilities leaders, and IT asset managers at the same time.

Once you understand how verification of assets works, the real challenge is putting it into action smoothly and at scale. That’s where a balanced approach makes all the difference—using software to capture mobile-based proof, track exceptions in real time, maintain audit trails, and integrate with your ERP, while also relying on expert services for baseline creation, asset tagging, annual verification, and multi-site execution. As a result, instead of treating verification of assets as a one-time activity, you turn it into a structured, repeatable process that actually works on the ground.

FAQs

Q1: Why is fixed asset verification important?

Ans: Fixed asset verification reduces register drift. It helps companies catch missing assets, duplicate records, wrong locations, unresolved disposals, and weak handovers before those issues affect audit, reporting, insurance, or planning.

Q2: Is fixed asset verification the same as asset tagging?

Ans: No. Asset tagging gives an asset a unique identifier, such as a barcode or RFID label. Verification uses that identifier, plus field evidence, to confirm that the record is accurate.

Q3: How is verification different from reconciliation?

Ans: Verification is the field activity. Reconciliation happens after fieldwork and resolves the differences between the verified facts and the book records.

Q4: How often should companies verify fixed assets?

Ans: The right answer depends on mobility, value, risk, and policy. High-value and high-movement assets usually deserve more frequent checks than low-risk fixed-location assets.

Q5: Who should own the process?

Ans: Finance should usually own policy, reporting outcomes, and approvals. However, operations, facilities, IT, site custodians, and internal audit should all have defined roles.

Q6: Can software replace physical verification?

Ans: No. Software improves planning, capture, and reconciliation. However, it does not eliminate the need for physical confirmation or approved alternative controls.

Q7: What discrepancies show up most often?

Ans: The most common issues include missing assets, wrong locations, and duplicate records. In addition, there are unrecorded additions and retired assets that are still on the books. Furthermore, damaged or obsolete assets are often present simply because no one has processed them properly.

")

")