Introduction

Your FAR can be arithmetically perfect and physically fictional at the same time. Depreciation runs on schedule, the GL ties out, yet no one can identify which machine on the floor matches the asset record in the FAR. Without consistent asset tags, and fixed asset tagging best practices, that gap between records and reality only widens. This guide is written for the people who own that problem: controllers, fixed asset accountants, and auditors.

In this guide, you will learn:

- What fixed asset tagging involves, how tags link physical assets to FAR records, and why unique identification strengthens audit evidence and financial accuracy.

- How to manage bulk-capitalized assets, parent-child asset structures, and three-way reconciliation between physical assets, the fixed asset register, and the general ledger.

- Why structured evidence capture, regulatory requirements, and controlled disposal workflows improve compliance, support audits, and maintain accurate depreciation throughout the asset lifecycle.

- How to implement a fixed asset tagging program by mapping assets, capturing verification evidence, resolving exceptions, and synchronizing validated records with enterprise systems.

What Is Fixed Asset Tagging?

Fixed asset tagging is assigning a unique physical identifier a barcode, QR, or RFID tag to each asset on the fixed asset register and linking the tag to that FAR record, so every book entry can be proven on the floor, and every floor asset traced to the books.

The definition carries a discipline-generic tagging skip: the linkage runs to a specific FAR line, not just to “an asset record.” That one-to-one mapping is what makes existence testable, discrepancies countable, and audits scan-led.

Why the FAR Fails Without Physical Identity

Most FARs hold strong financial fields cost, capitalisation date, asset class, depreciation keys and weak physical ones. The asset itself often carries no durable ID, and the register no photo, serial, precise location, or named custodian.

So teams identify assets by description, invoice text, or memory. “HP laptop – Finance dept” matches forty machines. “CNC machine – Plant 2” matches twenty. Verification of any one of them is guesswork dressed as testing.

Tagging fixes the root cause: it gives each FAR line exactly one physical counterpart that can be scanned in seconds. Everything else in this guide builds on that mapping.

Ghost Assets and Unrecorded Assets: The Two Failure Modes

An untagged estate fails in two directions at once – and each direction needs its own verification pass:

- Ghost assets (in the books, not on the floor). Disposed, scrapped, or lost assets that still sit in the FAR – generating depreciation, insurance premiums, and tax cost. Found by file-to-floor verification: start from the register and locate every line physically.

- Unrecorded assets (on the floor, not in the books). Expensed purchases, project transfers, or migration casualties that were never capitalized. They sit uninsured and uncontrolled. Found by floor-to-file capture: scan everything present and match it back to the FAR.

Run only one direction, and you stay blind to half the problem. A complete tagging program supports both, because a scan is only meaningful when the tag maps to exactly one register record.

Tagging Bulk-Capitalized Assets: The “100 Chairs” Problem

Open any mature FAR, and you’ll find them: “100 chairs – $12,485.” “Office equipment – $85,000.” “Server rack items.” One line, many physical objects, zero individual accountability.

Bulk lines can’t be tagged one-to-one, so choose one of two treatments per line:

- Unit-map under the parent: issue 100 tags (FUR-CHR-0001 to 0100), each mapped back to the parent FAR line. Depreciation stays booked in total; physical accountability becomes individual.

- Split the line: where accounting policy permits, break the bulk entry into individual FAR lines, each with its own tag, cost allocation, and life. Cleaner long-term, heavier one-time effort.

Either way, decide the treatment for every bulk line before fieldwork starts. Discovering the “100 chairs” problem mid-campaign is how tagging projects stall on the floor.

Component and Parent-Child Tagging

The opposite problem also exists: one physical asset that should have several records. Production lines, HVAC systems, lab installations, and IT infrastructure often require hardware asset tagging so individual components can be identified despite having different useful lives, maintenance histories, and replacement cycles.

The treatment is a parent-child structure. The parent asset carries a tag; significant components carry their own tags, mapped to ERP sub-numbers or child records. Each level records its own make, model, serial, and condition.

Component replacement posts against the component, not the whole line; useful-life reviews work at the level where lives actually differ; and impairment indicators attach to the piece that’s actually impaired.

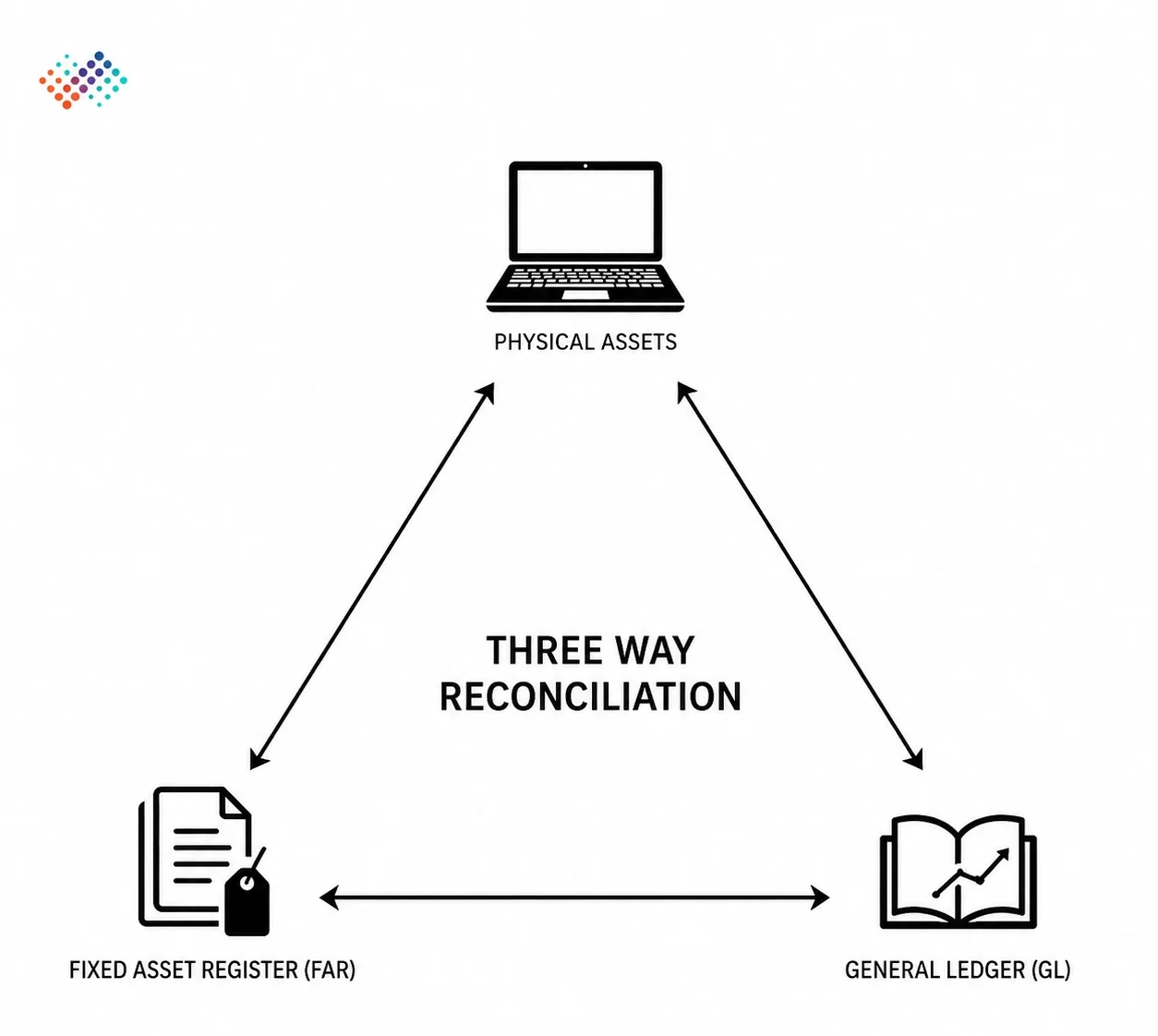

Three-Way Reconciliation: Physical, FAR, and GL

Tagged data earns its keep at reconciliation. Three sources must agree: the physical assets on the floor, the fixed asset register, and the general ledger balances.

Tagged data earns its keep at reconciliation. Three sources must agree: the physical assets on the floor, the fixed asset register, and the general ledger balances.

Tags make the first joint testable – every physical count resolves to specific FAR lines, so differences become countable exceptions instead of arguments. The FAR-to-GL joint is then a control-account tie-out, with approved corrections posted through an audit trail. A well-designed asset tagging system makes this reconciliation repeatable across multiple locations.

Evidence That Satisfies Auditors

A spreadsheet column that says “verified” proves nothing. Auditors accept evidence that answers five questions per asset: who verified it, when, where, in what condition, and against which unique identity.

A tagged estate produces that evidence as a by-product of scanning:

- Scan record – The tag ID, resolving to one FAR line.

- Photo – The asset as found, validated by AI against the expected asset type.

- Geolocation and timestamp – Where and when the scan happened.

- Verifier identity – Who performed it, under user-level logs.

- Approval history – How any discrepancy was classified, reviewed, and resolved.

Design the program so this evidence accumulates automatically. Audit season then becomes an export, not a scramble.

What This Looks Like in Practice: Four Field Cases

- The lumped line: A FAR entry “Office equipment – $43,689” turned out to be 118 physical items across three floors. Unit-mapping under the parent line gave each item a tag and a custodian without touching the depreciation booked in total.

- The production line: One FAR line, fourteen significant components with lives from 5 to 25 years. Parent-child tagging against ERP sub-numbers let component replacements post correctly for the first time.

- The ghost server room: A decommissioned rack estate still depreciating two years after removal. File-to-floor verification evidenced the absence; the approved write-offs cleaned both the FAR and the insurance schedule.

- The identical machines: An auditor sampling 20 near-identical CNC machines had previously accepted “one of these is line 214.” Unique tags ended the ambiguity – each sample resolved to one line, one scan, one photo.

Different industries, one pattern: the accounting was never the problem. The missing piece was a physical identity the accounting could point to.

Compliance Context by Market

Regulators rarely say “apply tags” – they say “prove your PPE,” and tagging is how proof scales. The expectations by the market:

Market |

Framework |

What it expects of the register |

| India | CARO 2020 Clause 3(i); Companies Act 2013 s.128 | Proper records with full particulars, quantitative details and situation of PPE; physical verification at reasonable intervals; material discrepancies properly dealt with in the books |

| Global (IFRS) | IAS 16; IAS 36 | Reliable carrying amounts, useful lives and residual values (IAS 16); assets not carried above recoverable amount condition evidence from tagging informs impairment review (IAS 36) |

| USA | ICFR / SOX-style controls; GAAP | Documented, repeatable evidence for existence and completeness assertions over fixed assets |

| UK | FRS-aligned audit practice | A maintained, verifiable register across estates; auditors test existence against unique identification |

| Australia / Philippines | AASB (IAS-equivalent) / BIR record-keeping and group audit alignment | Same substance: identifiable assets, periodic verification, discrepancies resolved with evidence |

The common denominator: Every framework assumes assets can be individually identified. Tagging is the assumption made real.

Disposal, Write-Offs, and Keeping Depreciation Honest

Ghost assets are usually disposal failures. The machine was scrapped in 2024; the FAR never heard about it; depreciation keeps running.

A tagged estate closes the loop:

- Disposal is evidenced: The final scan and photo document the asset leaving service.

- Approval precedes posting: Write-offs and retirements route through workflow, then post to the ERP.

- The tag number retires with the asset: Permanently. Reusing it merges two assets’ histories and corrupts the audit trail.

Run the same discipline for found ghost assets: evidence the absence, approve the write-off, post the retirement. The FAR gets lighter and truer at the same time.

How to Tag Fixed Assets Against the FAR: 8 Steps

- Export and clean the FAR: remove duplicates, flag zero-NBV lines, and identify every bulk-capitalized entry.

- Decide the unit-of-tagging per FAR line: one-to-one, unit-mapped under a parent, or parent-plus-components.

- Establish an asset tag numbering format, assign unique tag IDs, and map each tag to its FAR record and to ERP sub-numbers where components exist.

- Physically tag with evidence capture: photo, condition, location, custodian, and geolocation at every asset.

- Run file-to-floor verification to prove every FAR line exists; queue missing assets as exceptions.

- Run floor-to-file capture to surface unrecorded assets; route them for capitalization or reclassification review.

- Reconcile three ways (physical, FAR, GL); post approved corrections with an audit trail.

- Enterprise asset tagging software can automate synchronization, verification workflows, reporting, and reconciliation across multiple locations.

Key Takeaway

- Implement fixed asset tagging by linking every physical asset to its corresponding FAR record; therefore, finance teams can validate existence, improve audit evidence, and maintain accurate depreciation records.

- Resolve ghost assets, unrecorded assets, bulk-capitalized entries, and component assets through structured tagging and reconciliation; consequently, organizations strengthen financial accuracy and improve fixed asset management controls.

- Capture scan records, photographs, locations, timestamps, and approval histories during verification to create reliable audit evidence that supports compliance, reconciliation, and informed impairment or disposal decisions.

- Establish governed mapping, three-way reconciliation, and controlled disposal workflows so physical assets, the fixed asset register, and the general ledger remain synchronized throughout the asset lifecycle.

Conclusion

Fixed asset tagging creates a reliable connection between physical assets and financial records, making every asset easier to identify, verify, and reconcile. By using durable fixed asset tags and following fixed asset tagging best practices, organizations strengthen audit evidence, reduce ghost assets, and maintain accurate depreciation records.

Moreover, consistent tagging, structured reconciliation, and governed disposal workflows keep the fixed asset register aligned with physical assets throughout the asset lifecycle.

Fixed Asset Tagging FAQs

Q1: Why do fixed assets need tags if they’re already in the ERP?

Ans: ERP records hold financial data but often lack reliable physical identity – no durable ID on the asset itself. Tags create the physical-to-digital bridge that makes existence, location, and condition verifiable.

Q2: Is fixed asset tagging mandatory in India?

Ans: Tagging itself isn’t named in law, but CARO 2020 requires proper PPE records with quantitative details and situation, physical verification at reasonable intervals, and treatment of material discrepancies – which is practically impossible to evidence at scale without unique tags.

Q3: How does tagging support depreciation and impairment decisions?

Ans: Condition and usage evidence captured at tagging and verification (photos, condition grades) informs useful-life, residual-value, and impairment reviews under IAS 16 and IAS 36, replacing assumptions with observed asset state.